You picked your activity, reserved a trade name, and lined up every document on the checklist. Then the status came back: rejected. Or it simply stalled at "pending", with no clear reason attached.

If that is where you are, two things are worth knowing straight away. Business license rejection in Dubai is far more common than most founders expect, and it is rarely a verdict on your business idea. In our experience handling rejected applications, most rejections trace back to something fixable. The problem is usually how the application was put together, not the business behind it.

And here is the part almost no online guide will tell you. In 2025 and 2026, a growing share of setup failures happen after the license is issued, at the banking stage, not before it. A clean trade license no longer guarantees a working company.

This guide explains what a rejection actually means, the real reasons applications fail in Dubai today, and the practical steps to prevent or recover from one.

| Question | Short answer |

|---|---|

| Is a rejection permanent? | Usually not. Most are recoverable once the root compliance issue is correctly diagnosed. |

| The #1 hidden cause? | Narrative inconsistency: your activity, documents, website and ownership not telling one coherent story. |

| Rejected vs pending? | Different statuses, different fixes. Pending means the authority still wants something; rejected means the application is closed. |

| Biggest 2026 risk? | Rejection at the banking stage, after the license is issued. |

| First move after a rejection? | Diagnosis, not resubmission. Rushing a fresh application usually repeats the mistake. |

Why do business license applications get rejected in Dubai?

Quick answer

Business license applications in Dubai are rejected mainly because of failed due diligence checks, incomplete or inconsistent documentation, an unclear ownership structure, or a business activity that does not match the applicant's real operations. Most rejections happen at the initial approval stage and are recoverable once the underlying compliance issue is corrected.

Dubai runs a structured licensing process: initial approval, trade name reservation, office or lease submission, signing the Memorandum of Association, license payment, any third-party approvals, and finally license issuance. Outright rejection almost always happens at the first stage. Approval also depends on more than the licensing authority alone. Dubai immigration (the GDRFA) and the relevant regulator, whether the Department of Economy and Tourism (DET) for mainland companies or a free zone authority, each apply their own checks. If any of them raises a concern, your application stops moving.

But the more useful question is what your application status actually means, because not every halt is a rejection.

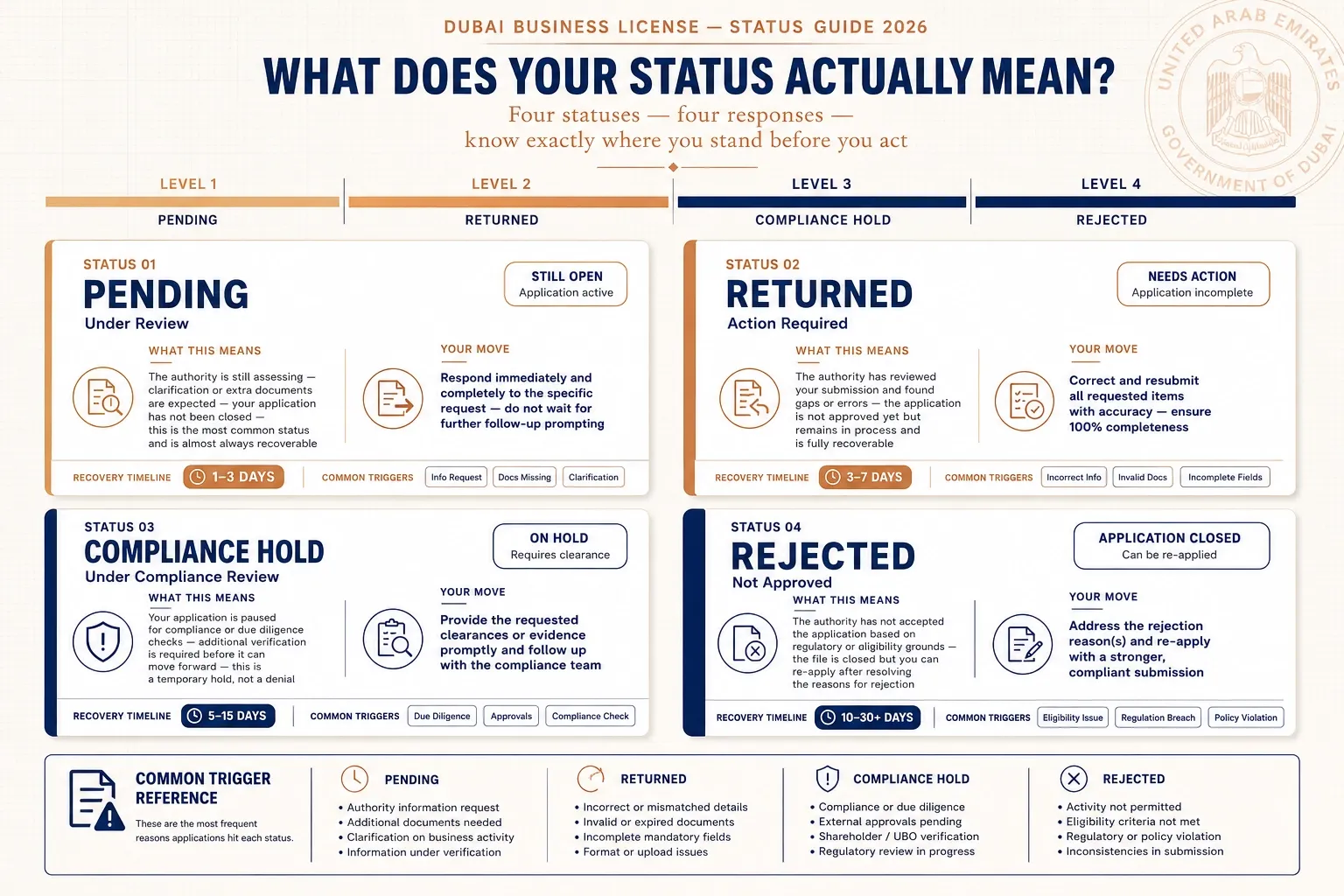

What "rejected" actually means: rejected vs pending vs compliance hold

Founders tend to read any non-approval as a rejection. In practice, authorities use several different statuses, and each one calls for a different response. Reading the status correctly is the difference between a three-day fix and weeks of wasted effort.

| Status | What it means | Typical fix |

|---|---|---|

| Pending / under review | The authority is still assessing and usually expects clarification or extra documents. | Respond quickly and completely to the specific request. |

| Returned for modification | A procedural issue, often a document error or wording mismatch. | Correct the flagged item and resubmit. Often recoverable in days. |

| Compliance hold | Enhanced due diligence has been triggered, often by ownership, nationality or activity risk. | Address the root compliance concern with full disclosure. |

| Rejected | The application is closed. | Diagnose the cause, restructure if needed, then reapply. |

A common and costly misconception is that every rejection is permanent. It is not. Many cases are recoverable, as long as the actual reason is identified before anything is resubmitted.

Is there a correction window in Dubai?

Yes, but it varies by authority, and there is no single national rule. DET mainland applications often allow a clarification or amendment window before a rejection status is finalised. Many free zones operate informal correction periods, where the application sits in "pending compliance review" rather than being closed outright. Rejections often resurface at trade licence renewal, so keep your documents current.

Because that window is discretionary and time-limited, speed matters. Our general manager puts it plainly:

Correction Window

A rejection notice isn't a dead end, it's a pivot point. Many licensing authorities provide a limited correction window, often around 30 days, subject to the authority's discretion. My instruction to our team is simple: act within the first 48 hours to rectify documents or clarify backgrounds, so clients never lose their momentum or their initial government fees

General Manager, Best Solution

The takeaway: do not wait for a formal, fully detailed explanation before you start working. The correction window may already be running.

The real reasons business licenses get rejected in Dubai

Most published lists stop at documentation errors. Documentation matters, but it is only part of the picture. Here are the reasons we see most often, including several that rarely make it into standard guides.

1. The wrong business activity

Dubai offers thousands of approved business activities across mainland and free zones, and each carries its own conditions, approvals and limits. Picking an activity that sounds close to what you do, rather than one that matches it, is one of the fastest routes to rejection. Authorities in 2026 cross-check your selected activity against your business description, your documents, your ownership structure, and even your planned banking activity. Choosing the right type of trade license walks through how the activity decision works. A clean licence record also makes it far easier to open a corporate bank account.

We worked with a European founder who applied for a standard marketing consultancy license on the Dubai mainland. During banking checks, the bank found a problem. The company's draft website and onboarding documents repeatedly mentioned crypto-payment routing and affiliate payout management. The licensed activity did not match the real operating model. The result was a bank rejection first, then licensing scrutiny. We restructured the activity mix and removed the restricted language from the public assets. Then we added the right third-party agreements and moved the client to a better-suited jurisdiction. Approval followed on resubmission.

2. Narrative inconsistency (the reason guides never mention)

This is the single most overlooked cause of rejection. Regulators and banks no longer assess one document at a time. They compare the whole picture: your license activity, your website wording, founder LinkedIn profiles, shareholder backgrounds, sample invoices, declared source of funds, nationality risk exposure, and even your hiring plans.

Applications are often rejected not because one document is missing, but because the overall commercial story does not logically hold together. A consultancy license paired with a website describing payment processing, or a small declared capital paired with a large projected turnover, creates exactly the kind of contradiction that triggers a closer look. If your application cannot tell one consistent story, expect questions.

3. Failed due diligence and background checks

Every applicant goes through due diligence, and free zones in particular run thorough background checks. These exist to satisfy anti-money laundering (AML) regulations and national security requirements, in line with FATF guidance. Many authorities screen applicants, shareholders and their connections through databases such as World-Check.

Past immigration issues, such as a previous visa overstay or a record of false documents, can trigger an immediate rejection. Unresolved legal or financial cases, anywhere in the world, can do the same. In one case we handled, an applying couple were flagged when a database surfaced a legal case linked to one spouse abroad.

Applicants holding certain nationalities, including Pakistani, Syrian, Jordanian, Algerian, Iraqi, Lebanese, Nigerian and Yemeni passports, may face enhanced verification. This does not mean rejection, and it is not a judgement on the individual. It means more documentation and a longer review. Dual citizenship can have the same effect if one nationality falls under enhanced scrutiny. In several cases, applying from within Dubai rather than from the home country has made the process noticeably smoother.

4. Incomplete or mismatched documentation

Missing or inconsistent paperwork remains one of the most common rejection triggers. The usual culprits: a passport with less than six months of validity, a missing tourist visa or Emirates ID copy, an absent tenancy contract or No Objection Certificate (NOC), or a business plan that was requested but not supplied. Some activities, including general trading and management consultancy, require a detailed business plan for Economic Substance Regulations (ESR) reasons.

The 2026 twist is verification. Authorities now check documents against each other far more closely than before. A name spelled differently across two documents, or a figure that does not reconcile, can stall the entire application.

5. Insufficient financial proof

Authorities want evidence that a business is real and funded, not a shell company. Missing bank statements, salary certificates or proof of investment can lead to rejection, as can a declared source of funds that does not add up.

There are legitimate workarounds when standard proof is unavailable. One applicant without a personal UAE bank account secured approval by submitting a financial support letter from a verified contact. The point is not to hide a gap, but to evidence it credibly.

6. Unclear ownership and hidden UBO

Dubai authorities now place heavy emphasis on ultimate beneficial ownership (UBO) transparency. Incorrect shareholder details, unclear shareholding ratios, missing partner documents, or ownership structures not permitted for a given activity all cause rejection or a request to restructure.

In 2026 we worked with a GCC-based investor who tried to structure ownership through layered foreign entities. The person who actually ran the business was not the declared shareholder. On paper the documents looked acceptable. But enhanced due diligence exposed a mismatch. The funding source, the person with management authority, and the real owner did not line up. The application was frozen at the compliance stage, before visa issuance. The fix was transparency: full UBO disclosure, revised shareholder agreements, notarised declarations, and a simpler ownership structure. The second submission succeeded.

7. Signature mismatch or suspected forgery

If an application signature does not match the passport, or appears altered, authorities reject it immediately. This is treated seriously. Under the UAE Penal Code, Federal Decree-Law No. 31 of 2021, forging an official document is a criminal offence that can carry imprisonment of up to ten years. This is not an area for shortcuts or "good enough" paperwork.

8. Trade name violations

A trade name has to follow UAE naming conventions. Names are rejected or held when they reference religion or divine attributes, resemble a well-known brand, include restricted or political terms, or do not reflect the licensed activity. A name that is already registered will also be refused. Until an acceptable name is approved, the application stays pending. Trade name registration rules in Dubai covers the naming rules in detail.

9. Missing third-party approvals and failed inspections

Some activities need approvals from bodies beyond the licensing authority before a license can be issued. A restaurant, for example, needs a No Objection Certificate from the Food Safety Department of Dubai Municipality, has to meet a minimum space requirement, and must pass a final inspection against the Dubai Food Code. Health, education and finance activities trigger their own regulators. Missing one of these approvals leaves the application stuck in pending status.

10. Office space and Ejari problems

Most businesses need a valid office address registered with the authorities. Mainland applications generally require a physical office. The lease must be attested by the Real Estate Regulatory Agency (RERA) and registered on the Dubai Land Department's Ejari system. A missing, mismatched or unregistered lease will hold up issuance. Requirements vary by activity and emirate, so the lease has to match the license, not simply exist.

11. Applying in the wrong jurisdiction

Dubai offers mainland, free zone and offshore structures, and each suits a different model. Many founders pick one on cost or speed alone. If the structure does not support your activity, visa needs and target market, the result is often rejection or forced restructuring. Applying for a free zone license while planning to trade directly in the mainland market is a classic mismatch. Mainland and free zone business setup compares the structures.)

Most Rejections Are Recoverable. Is Yours?

Most Dubai license rejections are recoverable — if you fix the right thing first. Get a free honest diagnosis from our team before you file again.

The 2026 risk no one warns you about: rejection after your license is issued

Here is the uncomfortable truth that the speed-focused setup ads will not mention: most UAE business setup failures now happen after the license is issued, not before.

A trade license proves the company exists. It does not prove the company can bank, invoice or operate. We worked with an online seller who received their trade license without any problem, then failed with several UAE banks. The license was fine. The banking file was not: inventory sourcing invoices, supplier history and logistics documentation were all too thin to satisfy the banks' checks. We rebuilt the file with supplier contracts, warehouse details, transaction-flow mapping and realistic turnover projections. Banking approval came through within weeks.

This is also why two pieces of popular advice are worth challenging.

"Choose the cheapest license and upgrade later" sounds efficient. In practice it often creates expensive downstream problems: banking rejection, VAT complications, payment gateway refusal, immigration scrutiny, or an inability to scale activities legally.

"Free zones approve everything faster" is only half true. Some free zones are quick to issue a license. But banks may then apply stricter scrutiny depending on the activity, the shareholder profile and economic substance expectations. Speed of issuance is no longer the right metric. Compliance compatibility is.

An increasing share of the recovery cases we handle in 2025 and 2026 involve banking-stage failure rather than trade license rejection itself. Plan for the bank before you apply for the license, not after.

How to avoid business license rejection in Dubai

The pre-submission checks that surprise people

A standard checklist covers passports, the tenancy contract and the business plan. A serious pre-submission review goes further. Before we submit an application, we check things most public guides never mention:

- Whether the proposed company name accidentally triggers banking compliance keywords.

- Whether the website wording could create a regulatory mismatch with the licensed activity.

- Whether projected revenue is consistent with the requested visa count and office size.

- Shareholder travel history and residency structure, where enhanced due diligence is likely.

- Whether the chosen activity combination creates hidden regulatory overlap.

- Whether invoice templates and future transaction descriptions will read as high risk to UAE banks.

- Whether the source-of-funds logic holds up before any authority asks for it.

Pre-Approval Risk Mapping

The thread running through all of those checks is simple: licensing, immigration and banking risks are connected, and they should be assessed together, before submission, not in sequence afterwards. We call this Pre-Approval Risk Mapping. Instead of treating the license as step one and the bank account as a later problem, it maps every likely point of friction across all three areas first, so the application is built to survive the checks it will actually face. Why license preparation matters explains the preparation stage.

What to do if your business license is rejected in Dubai

The first 48 hours: diagnosis, not resubmission

The instinct after a rejection is to fix the obvious thing and resubmit fast. That instinct is usually wrong. Resubmitting before you understand the real cause tends to reproduce the rejection.

The first 48 hours should go to diagnosis. Our team works through four reviews in that window:

- Compliance audit. Read the rejection notes, authority comments, any banking feedback and the full application history.

- Narrative alignment review. Compare the activity, ownership structure, online presence and intended transactions for contradictions.

- Jurisdiction suitability check. Decide whether the issue is fixable within the same authority, or whether the jurisdiction itself is the problem.

- Risk escalation mapping. Assess whether the case triggered enhanced due diligence because of nationality exposure, a regulated activity, sanctions proximity, crypto involvement or unexplained fund flows.

Often the correction work begins before the authority has even issued its full written explanation.

Fix and resubmit, or move to another emirate?

Reapplying in a different emirate is sometimes the right call, and sometimes a way to repeat the same rejection somewhere new.

Move when the authority itself is unsuitable for the activity, when the activity sits in a compliance gray zone, when banking acceptance is structurally weak in that jurisdiction, or when the operating model conflicts with local regulatory expectations.

Fix and resubmit in the same jurisdiction when the issue is documentation-based, when ownership clarification is enough, when activity wording can be corrected, or when the rejection came from a procedural inconsistency rather than a risk profile.

The rule underneath both: changing emirates without solving the underlying compliance problem usually just relocates the rejection.

How long recovery takes, and how often it works

For cases our team takes on after review, the resubmission success rate is typically in the range of 70 to 85 percent, depending on the rejection category. Rough timelines:

• Simple correction cases: 3 to 7 working days.

• Activity mismatch cases: 1 to 3 weeks.

• UBO or compliance restructuring: 2 to 6 weeks.

• Banking-related recovery: often longer than the licensing itself.

The most recoverable cases are wrong activity selection, incomplete compliance documentation and weak banking files. The hardest are undisclosed beneficial ownership, sanctions exposure, a fabricated source-of-funds explanation, or any attempt to conceal what the business actually does. Honesty is not just ethical here. It is the single biggest factor in whether a case can be saved.

Conclusion: rejection is rarely the end of the road

Dubai's licensing rules are strict, and in 2026 they are more interconnected than ever, with licensing, immigration and banking checks all reading from the same story. That is exactly why a rejection feels alarming, and why it is so often recoverable.

A rejection is rarely a verdict on your business. It is usually a signal that the application did not yet tell one clear, consistent, compliant story. Diagnose the real cause, fix it properly, and most applications can move forward.

if your application has been rejected or stalled

Get an honest diagnosis

Best Solution handles rejected and stalled applications across Dubai's mainland and free zones. If your license has been refused, or has stalled at pending, the fastest first step is an honest diagnosis of why. Book a free consultation and we will tell you whether your case is fixable, and what it would take