Most founders in Dubai treat tax as something to handle once revenue arrives. The structure that decides your tax position is set earlier, at incorporation. It is expensive to change later. The UAE went from a near-zero-tax reputation to an active corporate tax and VAT regime in under three years. The 0% rate that free zones are famous for is now a conditional outcome you maintain. It is not a permanent setting you switch on at licensing.

This guide covers the five corporate tax structuring decisions that shape your liability for years. Each one is cheap to get right at setup and costly to retrofit later. The figures and client situations here come from Best Solution's own files. We are an FTA-registered Tax Agent, operating from Business Bay since 2014. We have supported 5,000+ company formations, 4,500+ corporate bank account applications, and 2,500+ AML and compliance filings. We have also documented more than AED 10 million in penalty reductions for clients who came to us after the structure had already gone wrong.

Tax Structuring in Plain Terms

Tax structuring is the set of choices made at incorporation that fix how a UAE business is taxed. It covers where the business is licensed, what entity type it uses, how it registers for corporate tax and VAT, and how it documents related-party transactions. These decisions are structural. Once revenue is flowing, changing them means new entities, amended contracts, and revised registrations. That is why fixing a structure always costs more than building it correctly.

At a glance

| Scenario | Headline Licence | Realistic Year-One Total |

|---|---|---|

| Free zone, solo founder, 1 visa | ~AED 12,000 - 15,000 | AED 22,000 - 35,000 (+80-150%) |

| Mainland, 5 employees, regulated | ~AED 15,000 | AED 60,000 - 100,000 (+150-300%) |

Decision 1: Free Zone Incorporation and the QFZP Test

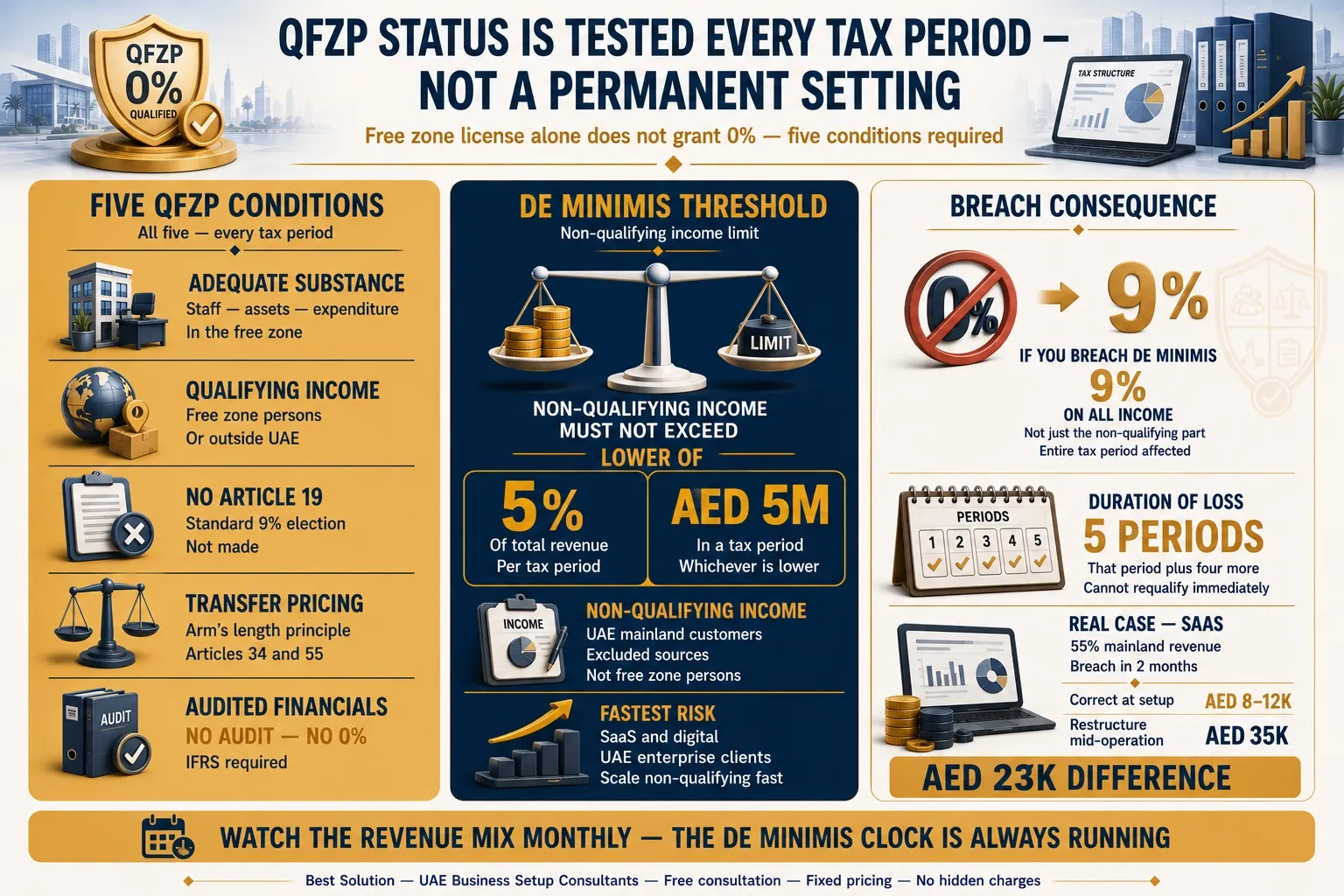

Incorporating in a free zone is the headline tax decision. It is also the one most often misunderstood. A free zone license does not grant a 0% corporate tax rate by itself. It gives you the chance to qualify for 0% on qualifying income. To get it, you must meet and maintain the conditions of a Qualifying Free Zone Person (QFZP). These sit in Article 18 of the UAE Corporate Tax Law, Federal Decree-Law No. 47 of 2022.

The most common and most expensive mistake we see is simple. Founders treat the 0% rate as unconditional and permanent. They assume it requires no active maintenance. The assumption runs: license issued, therefore 0% tax, therefore nothing further to do. In reality, QFZP status is tested every tax period.

The five QFZP conditions

To be a Qualifying Free Zone Person and keep the 0% rate on qualifying income, an entity must:

- Register in a UAE free zone and maintain adequate economic substance. Its core income-generating activities must happen in the zone, with enough staff, assets, and expenditure.

- Earn qualifying income. This is broadly income from other free zone persons and from qualifying activities with parties outside the UAE.

- Not elect to be taxed under the standard 9% regime under Article 19.

- Comply with the arm's-length principle and transfer pricing rules under Articles 34 and 55.

- Prepare audited financial statements under IFRS.

A sixth practical condition runs across the others: stay within the de minimis threshold for non-qualifying income. On the audit point, the FTA position is blunt, and it is worth stating plainly. No audit, no 0%. A company that claims QFZP status without audited financials has no defensible claim.

The de minimis test most founders never check

Non-qualifying income is broadly income from mainland UAE customers and other excluded sources. It must not exceed the lower of 5% of total revenue or AED 5 million in a tax period. Cross either threshold and you lose QFZP status. The damage is not limited to the non-qualifying portion. You lose 0% on all income for that period, and for the next four tax periods.

This is where free zone businesses are caught during growth, not at launch. One pattern recurs in our files more than any other. SaaS and digital services companies with UAE enterprise clients trip the de minimis test fastest. A B2B product that gets traction with UAE mainland corporates scales its non-qualifying revenue faster than any other model. A product at 20% mainland revenue in month six is often at 50% by month eighteen. That is exactly when the founder is focused on sales, not tax structure.

Client case: the cost of the “free zone = 0%” assumption

A free zone SaaS company came to us eight months after incorporation. Another consultancy had set them up on the standard "free zone equals 0% tax" assumption. By then their revenue split was 55% UAE mainland corporate clients and 45% international. The mainland revenue was non-qualifying. At their growth rate, they would breach the de minimis threshold within two months. We mapped three options. They could elect out of QFZP voluntarily, restructure with a mainland operating entity to ring-fence the UAE-facing revenue, or re-route the mainland invoicing through a correctly positioned entity. They chose a dual-entity structure: a free zone entity for international revenue, and a mainland LLC for UAE corporate clients. The restructure took six weeks. It cost roughly AED 35,000 in new entity setup, amended contracts, updated bank accounts, and revised VAT registration. Had the structure been correct at incorporation, the mainland entity would have cost AED 8,000 to AED 12,000 to add. The AED 23,000 difference is the price of the "free zone equals 0%" assumption.

One detail competitors rarely mention: the bank often surfaces the QFZP risk before the tax authority does. During account opening, the bank reviews your declared activity against your real transaction flow. A free zone entity licensed for "software development" but receiving a stream of UAE mainland invoices triggers a query. The transaction narrative does not match the free-zone-to-international model that justifies the structure. We now treat that bank question as an early warning signal. If the bank asks why a free zone company is invoicing UAE mainland entities, the tax structure needs review at once.

For a deeper comparison of the two licensing routes, see our guide on free zone versus mainland in Dubai.

Decision 2: Register for VAT From Day One

VAT is the obligation founders most often defer. They assume low early revenue means no liability. The mandatory VAT registration threshold is AED 375,000 in taxable supplies and imports over any rolling 12-month period. It is set by Federal Decree-Law No. 8 of 2017. Once you cross it, you have 30 days to file your registration with the Federal Tax Authority through EmaraTax. Miss that window and the late registration penalty is AED 10,000, under Cabinet Decision No. 49 of 2021. We have seen clients pay more in VAT penalties than they paid for their trade license.

The threshold is a rolling figure, not an annual one. A services or trading business that hits AED 375,000 in month five has triggered the obligation. It does not matter whether anyone was tracking it. There is also a voluntary registration option at AED 187,500. It is worth considering before you are obliged. Early registration lets you recover input VAT on startup costs and issue compliant invoices from the first transaction.

For multinational and B2B founders, early VAT registration is also a credibility signal. It lets you structure contracts cleanly and recover input tax on setup spending. It tells corporate clients the business is built for proper governance, not scrambling to backfill registrations later. If you are unsure where you stand, our VAT registration and filing service handles the threshold assessment and EmaraTax filing.

Decision 3: Choose an Entity Structure That Survives Cross-Border Reporting

Founders tend to obsess over local compliance. They underweight how their UAE entity interacts with international tax systems. The entity structure you choose at incorporation drives your exposure to cross-border reporting, profit repatriation rules, and the disclosure obligations of other countries. This matters most for two groups. The first is founders with US persons in the cap table. The second is founders who plan to raise institutional capital.

A UAE free zone company is well understood by GCC investors and family offices. US and EU institutional investors often expect a familiar holding structure above the UAE operating company. Retrofitting that after a funding round is far more disruptive than designing it at the start. The same logic applies to founders who stay tax-resident or reporting-connected elsewhere. A UAE entity that is efficient locally can still create a reporting headache abroad if the structure ignored that side.

The lens we apply to every structuring decision is audit defensibility. The question is not only what lowers your tax bill this quarter. It is what entity classification will withstand five years of international reporting and scrutiny from revenue authorities. That single decision, made at incorporation, is often the line between scalable growth and a tax position no relief program can fully unwind. For the structural options, see our guide to types of business and company structures in the UAE .

Decision 4: Design for Treaty Benefits and Economic Substance

The UAE has one of the world's largest double taxation treaty networks. Access to those benefits is not automatic. It depends on your incorporation jurisdiction, your entity type, and whether you can demonstrate genuine substance. Many investors rush into a free zone structure for the incentive alone. They do not check whether their activities will trigger onshore VAT or corporate tax exposure. They also do not check whether the structure can actually claim treaty relief when it matters.

Substance is the pivot. The QFZP regime and most treaty positions require that your core income-generating activities genuinely happen in the UAE. That means real staff, premises, and expenditure. Here free zone selection has a hidden tax consequence. The larger, established zones such as DMCC, DIFC, and JAFZA have well-documented substance frameworks. Some smaller and budget zones have less guidance on what counts as adequate substance. A company that picks a low-cost zone purely on price can later hit a wall. The zone's infrastructure may not support the documentation a corporate tax audit would require. The cheapest free zone setup is occasionally the most expensive tax structure.

The rule we give clients is direct. Design around substance and cross-border alignment, not around the headline incentive. A structure built on substance from day one avoids costly restructuring later. It also keeps the door open to legitimate treaty efficiencies. Choosing the right activity scope is part of this. Our guide on how to choose your business activity in Dubai covers how activity selection feeds the regulatory and tax pathway.

Decision 5: Transfer Pricing Documentation From the First Related-Party Transaction

This is the decision most founders never realise they have made. It is the one we would add to the standard list. UAE corporate tax law requires that transactions between related parties and connected persons be priced at arm's length. Arm's length means the price unrelated parties would agree. The rule sits in Articles 34 and 55 of Federal Decree-Law No. 47 of 2022. The obligation exists from the first transaction, not from a later revenue milestone.

It sounds like a large-company problem. It is not. A UAE free zone company that invoices a related entity abroad has a related-party transaction. So does one that pays a management fee to a parent or lends to a sister company. Each needs an arm's-length pricing position and the records to support it. Documentation scales with size. A Transfer Pricing Disclosure Form is required where related-party transactions exceed AED 40 million in a tax year. Full master file and local file documentation applies to large groups above defined revenue thresholds. But the arm's-length principle itself applies to everyone from day one. Documentation failures carry penalties starting at AED 50,000. After that, the FTA can adjust your prices and add tax owed plus a further penalty.

For founders with a parent company, a related entity abroad, or intra-group invoicing, a simple transfer pricing policy set at incorporation is inexpensive. Reconstructing one under audit, years of transactions later, is not.

The Pattern Behind Every Expensive Mistake

Read back through these five decisions and the same root cause appears: deferral. "I'll sort the tax side out once the business is making money" is the most common and most expensive sentence in the market. The logic is understandable. A pre-revenue founder does not want to spend on tax advice before there is tax to manage. The flaw is structural. The decisions that determine tax efficiency are made at incorporation. A free zone entity set up with the wrong activity scope, the wrong related-party structure, or no VAT plan cannot be cheaply retrofitted once revenue flows.

A close second is "my accountant back home handles this." UAE corporate tax law is specific to this country. So are the QFZP conditions, the de minimis test, the substance requirements, and the EmaraTax system. A competent accountant in London, Mumbai, or Berlin does not automatically know how Article 18 interacts with a mixed-revenue free zone entity. We regularly see the result. Clients arrive after their home-country adviser filed a UAE return incorrectly or missed a UAE-specific obligation.

A useful test cuts through all of it. Where will roughly 80% of your first-year revenue come from? If the answer is UAE mainland customers, a pure free zone structure built for international revenue is already misaligned, and the de minimis clock is running. If the answer is international clients, the free zone structure fits. But it only holds if you maintain substance and watch the revenue mix as you grow. The structure should follow the revenue. The revenue should be honestly forecast.

Why Structuring at Incorporation Costs Less Than Restructuring

Every figure in this guide points the same way. The mainland entity that costs AED 8,000 to AED 12,000 at setup costs AED 35,000 to add mid-operation. The VAT registration that is free to file on time costs AED 10,000 once it is late. The transfer pricing policy that is a modest exercise at incorporation becomes a AED 50,000 exposure when it is missing under audit. Structuring is cheap. Restructuring is not.

What qualifies us to make these calls is the full compliance lifecycle in house. We handle corporate tax registration, EmaraTax filing, VAT registration and quarterly returns, transfer pricing documentation, and AML compliance. That is backed by FTA Tax Agent status. It lets us represent clients directly before the Federal Tax Authority on corporate tax and VAT matters. Not every setup consultancy holds that registration. Every client we have incorporated since June 2023 has needed corporate tax registration as a mandatory step, so our CT registration volume tracks our formation volume directly. Our compliance team is led by Teena Thomas, who has more than seven years in financial oversight and AML. She sees the failure patterns before most founders know they exist.

One timing note for 2026. Businesses with a financial year ending 31 December 2025 must file their second corporate tax return on EmaraTax by 30 September 2026. Small Business Relief is available only for tax periods ending on or before 31 December 2026. If you rely on either, confirm your dates now rather than at the deadline.

Incorporate in a Free Zone

If I were advising a business incorporating in Dubai today, the one tax structuring choice I’d treat as non-negotiable is choosing to incorporate within a Free Zone, especially one that fully aligns with the UAE’s new corporate tax and VAT frameworks. The implications of incorporating in a Free Zone are huge and offer many tax advantages, such as exemptions or lower rates, easier registration processes, and clearer audit paths. We’re seeing a rise in compliance obligations and scrutiny as a vital change, in part due to Dubai’s shift to corporate tax and VAT. I strongly recommend securing the right Free Zone status at the start to avoid surprise expenses, reduce paperwork, and keep your business agile, with the flexibility to reinvest savings into growing your business.

Owner, Omaha Home Advisors

Design Structure for Treaty Benefits

The one non-negotiable tax structuring decision in Dubai today is ensuring that the company’s incorporation jurisdiction and entity type qualify for treaty benefits and legitimate tax efficiencies from day one. Many investors rush to register under the Free Zone model without considering whether their activities will trigger onshore VAT or corporate tax exposure. At Elsabbah Law Firm, we advise clients to design their structure around substance and cross-border alignment, not just incentives. A well-planned incorporation avoids costly restructuring later and positions the business to benefit from double taxation treaties while staying fully compliant with the UAE’s evolving tax regime.

Law firm Founder & Managing partner , Elsabbah Law firm

Register for VAT from Day One

I would never skip registering for VAT from day one, even if the business projects limited revenue initially. In Dubai, the threshold often tempts founders to delay, but that decision creates messy retroactive filings and weakens credibility with partners who expect compliant invoices. Early VAT registration meant I could structure contracts cleanly, recover input tax on startup costs, and avoid scrambling later under FTA audits. It also signalled to clients—especially multinationals—that we were set up for proper governance. Corporate tax planning is important, but VAT is transactional, visible on every invoice, and can erode trust quickly if mishandled.

Co-Founder & CEO, AIScreen

Choose Entity Structure for Global Compliance

As a U.S. tax attorney, I’ve seen too many businesses collapse under the weight of tax mistakes made on day one. With Dubai’s corporate tax and VAT now at the center of its incorporation landscape, the single non-negotiable step is choosing an entity structure that aligns with cross-border reporting rules.

Entrepreneurs often obsess over local compliance, but what drains them later is how their Dubai entity interacts with international tax treaties, disclosure obligations, and profit repatriation.

In the U.S., I’ve worked with clients who saved six figures simply because they picked a structure that allowed them to legally shift the timing of deductions and credits. Without that foresight, those same clients would have been flagged for double taxation exposure.

The UAE is positioning itself as a global hub, but global hubs attract global scrutiny. Just look at how the IRS aggressively audits foreign-connected businesses. Last year alone, nearly 30 per cent of offshore audits uncovered recordkeeping flaws tied to entity choices.

In our practice, we stress “audit defensibility” as the lens for all structuring decisions. My tip for founders in Dubai: don’t just ask what lowers your VAT bill this quarter; ask what entity classification will withstand five years of international reporting and scrutiny from revenue authorities. That decision, made at incorporation, is often the dividing line between scalable growth and a tax mess that no relief program can fully unwind.

Partner, Tax Law Advocates

Quick reference: five things to confirm before you incorporate

Before you incorporate, confirm five things. First, whether your revenue mix lets you maintain QFZP status and stay under the de minimis threshold. Second, your VAT registration trigger date and whether voluntary registration helps. Third, an entity structure that survives cross-border reporting. Fourth, genuine substance in a zone whose framework supports an audit. Fifth, an arm's-length policy for any related-party transactions. Get these right at setup and the 0% rate, where you qualify, is defensible. Defer them and the relief programs cannot fully unwind the result.

Best Solution Business Setup Consultancy is an FTA-registered Tax Agent in Business Bay, Dubai. We structure businesses for tax efficiency at incorporation and handle the full compliance lifecycle afterward. To pressure-test your structure before you commit, talk to our business setup consultants in Dubai .