Most new businesses in the UAE do not fail because the idea was wrong. They fail because the money ran out first. A company can look profitable on paper and still miss payroll. Profit and cash are not the same thing. The gap between them is where new founders get caught.

This guide covers cash flow management for a UAE business in its first year or two. It explains what cash flow management is. It shows the banking choices that quietly cause cash flow problems months later. It also covers how to open your accounts so they are approved the first time, how much cash to keep in reserve, and how forecasting keeps you ahead of trouble.

The angle here is banking. That is where most cash flow problems in the UAE begin. This is not a guide to personal finance, investments, or accounting for large corporations. If your trade licence has just been issued, or it soon will be, this is the order of decisions to get right.

| Key Point | Why It Matters |

| Cash Flow ≠ Profit | Profitability does not guarantee liquidity. Businesses often fail because they run out of cash despite showing accounting profits. |

| Banking Decisions Matter | Poor banking setup choices frequently create operational and cash-flow bottlenecks during the first year. |

| Open Banking Early | Starting the bank account process immediately after licensing helps avoid delays in receiving payments and managing expenses. |

| Build Reserves | Maintaining dedicated reserves for expenses, VAT, tax liabilities, and payroll protects business continuity. |

| Keep It Simple | A single, well-managed business account is usually sufficient during the early stages of growth. |

What is cash flow management, and why does it decide whether new businesses survive?

Cash flow management is the process of tracking, forecasting, and controlling the money moving in and out of a business. The goal is simple: always have enough cash to meet your obligations. For a new company, it is the difference between paying staff and rent on time and stalling, no matter how profitable the business looks.

Why 82% of Businesses Fail in Dubai

Poor cash flow kills more businesses than bad products ever will. Structure your UAE banking correctly from day one or risk becoming part of that statistic.

The lesson is not that cash flow is complicated. It is that cash flow stays invisible until it becomes urgent. By then, the options left are usually the expensive ones.

Cash inflows, outflows, and the three places cash moves

Accountants split business cash into three types. Knowing them helps you read your own numbers. Operating cash flow is money from day-to-day trading: customer payments in, supplier and salary payments out. Investing cash flow covers one-off moves, such as buying equipment. Financing cash flow covers loans, owner capital, and repayments. For a new business, watch operating cash flow every week. It turns negative first, and it is the one payroll depends on.

Why the UAE's low-tax reputation makes founders complacent

The UAE's low-tax reputation creates a quiet trap. Many founders assume that a light tax burden means financial discipline matters less. So they run business spending through a personal account and plan to fix the structure later.

That assumption is now out of date. VAT arrived in 2018 and corporate tax in 2023. Every business now needs clean, separate records of what it earned and what it owes. In Best Solution's experience, mixing personal and business transactions in one account causes the most trouble at the first tax filing or bank review. Untangling several months of blended transactions is slow and error-prone. Sometimes it cannot be done in full.

The banking mistakes that cause cash flow problems in the first year

Most cash flow problems in a new UAE business are not bad luck. They are the delayed cost of a setup decision, made when banking felt like a box to tick. Three mistakes cause most of them.

Mistake 1: Running the business through a personal account

Using a personal account for business is technically allowed in the UAE. That is exactly why so many founders do it. The risk shows up later. Tax registration and filing need clear records of every business transaction. When business income and personal spending share one account, separating them after several months is a slow, manual job. It also weakens the business when it finally applies for its own account, because the bank has no clean trading history to assess. A dedicated business account from day one is not red tape. It is the foundation every other financial control sits on.

Mistake 2: Choosing a fintech-only platform over a traditional bank

Fintech platforms such as Wio, Wise, and Payoneer look appealing at setup. The account-opening process can feel faster and cheaper than a traditional bank. For some businesses, they work well. But they can also limit you later. Not all of them offer the full range of banking services, a dedicated relationship manager, or branch access for a complex transaction. For a business that plans to operate and grow in the UAE for years, Best Solution usually guides clients toward an established traditional bank as the main account. Fintech tools then act as a supplement, not the backbone.

Mistake 3: Picking a high-risk licence activity without thinking about banking

This mistake stays hidden until the account application is submitted. Banks treat certain business activities as high risk. A high-risk label makes opening a corporate account much harder. The decision that triggers it is made earlier, at company formation, when the licence activities are chosen. Often, a business could have picked a closely related activity in a lower-risk category and avoided the friction. So licence activities should be checked with banking in mind, not just operational fit. For help matching activities to risk level, see our trade licence activities guide before filing.

How to set up your business banking the right way

The order of these steps matters. Done in sequence, with documents ready in advance, account approval is usually smooth. Done reactively, the same process becomes the business's first cash flow crisis.

Step 1: Open the account as soon as your licence and Emirates ID are issued

Do not wait. Once the trade licence and Emirates ID are in hand, start the corporate account application. Every week without your own account is a week of transactions you will later have to explain or reconstruct.

Step 2: Choose the bank around your actual business

The right bank depends on your business activity, your transaction type and volume, and your growth plans. It does not depend on which account was quickest to open. For most new businesses, one account with a reliable traditional bank, such as Emirates NBD or Mashreq, is the right main choice. Many UAE banks now offer zero-balance corporate accounts. That removes the minimum-balance pressure that used to tie up working capital.

Step 3: Prepare the complete document set before you apply

Banks approve quickly when the file is complete, accurate, and consistent. A misspelled name or a missing statement can stall the whole process. Gather every required document before you apply, not during. The full checklist follows these steps.

Step 4: Present the business clearly to the bank

Documents alone do not secure approval. The bank's compliance team needs to understand three things without digging: what the business does, the expected volume and type of transactions, and the source of funds. A business that explains these clearly is far easier to approve.

Step 5: Keep personal and business banking fully separate

Once the account is open, hold the line. Personal expenses do not belong in the business account. Business income does not belong to a personal one. This one discipline keeps VAT and corporate tax filing clean. It also keeps the account in good standing during reviews.

Step 6: Set up forecasting from the first month

An account is infrastructure, not management. From month one, track expected cash in and cash out. That way, pressure is visible weeks before it arrives. The next section shows how.

- Trade licence

- Memorandum of Association (MOA)

- Office tenancy contract / Ejari

- Emirates ID

- Passport copy

- Last 6 months' personal bank statement

- Basic CV or LinkedIn profile

- For any other company owned in the UAE or abroad: its trade licence and last 6 months' bank statements

- KYC information and supporting details

In Best Solution's experience, about 90% of client applications are approved on the first attempt. The corporate account usually opens within one to two weeks. The difference between that and a long rejection is almost always preparation.

Get your UAE business banking right from day one

23 years. 5,000+ businesses. 90% first-attempt bank approval. We set up your banking before cash flow becomes the problem.

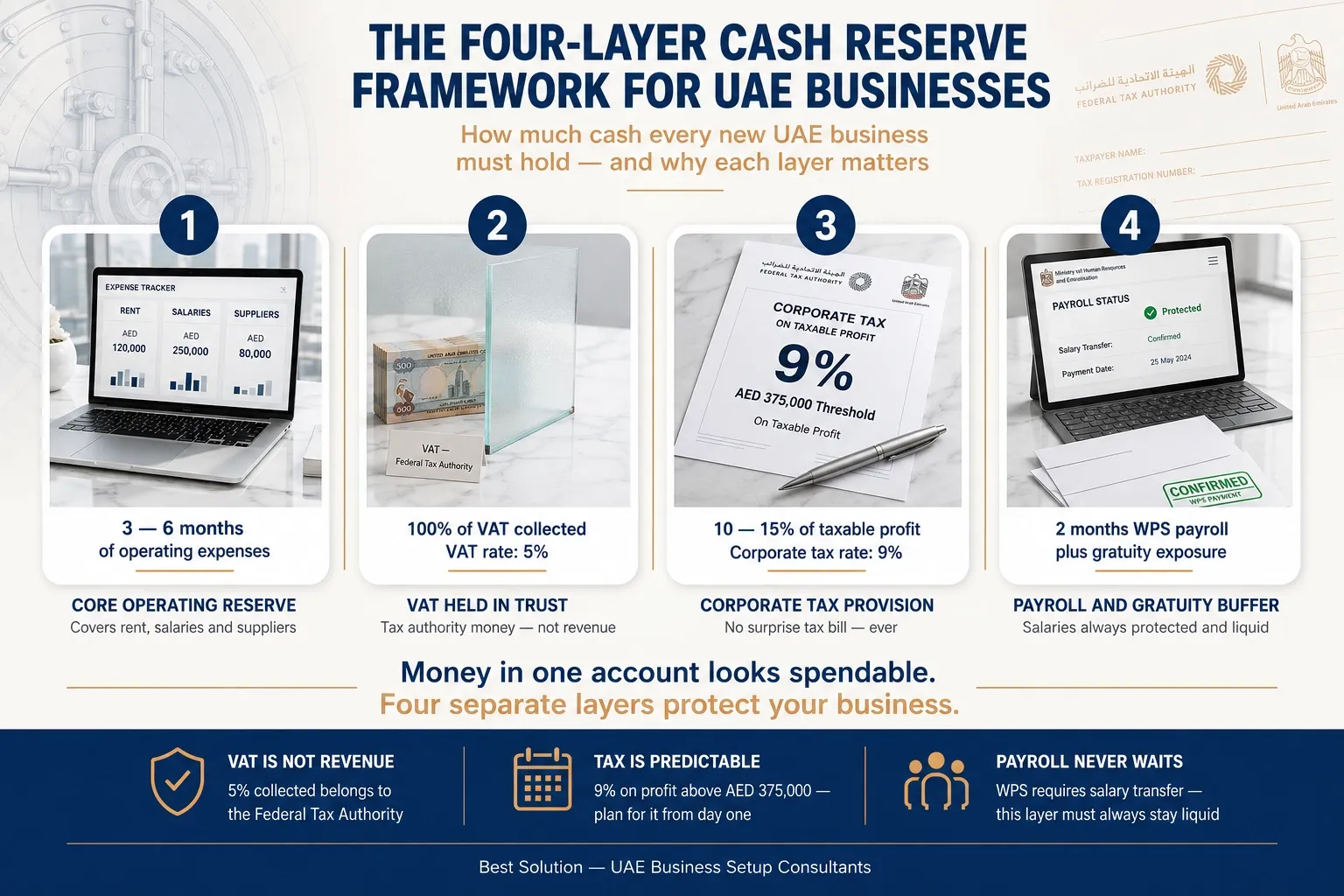

How much cash should a UAE business keep in reserve?

Generic advice says to keep three to six months of expenses in reserve. That is not wrong, but for a UAE business it is incomplete. It ignores three obligations that are neither optional nor yours to spend: VAT you have collected, corporate tax you will owe, and payroll you must pay through the Wage Protection System. Treating any of those as spare cash is a common way a profitable UAE business ends up short.

The Best Solution cash reserve framework

Best Solution advises new UAE businesses to hold reserves in four separate layers, not one pooled balance.

| Reserve Layer | What to Hold | Why it Matters |

| Core Operating Reserve | 3 to 6 months of operating expenses | Covers rent, salaries, and suppliers during slow periods or delayed customer payments. |

| VAT Held in Trust | 100% of VAT collected from customers | VAT is not revenue; it belongs to the tax authority and must be fully available at filing time. |

| Corporate Tax Provision | 10 to 15% of taxable profit | Ensures funds are ready for the 9% corporate tax obligation without cash pressure. |

| Payroll & Gratuity Buffer | At least 2 months of WPS payroll plus gratuity exposure | Protects salary obligations and end-of-service liabilities in liquid cash. |

Separating the layers is a safeguard for how you think, not just how you bank. Money sitting in one account looks spendable. The VAT layer and the tax provision are not. Hold the liabilities in a clearly labelled balance, or a separate account. Then the business never mistakes a future tax bill for working capital.

Corporate tax in the UAE is 9% on taxable income above AED 375,000, with a 0% band below that, according to the Federal Tax Authority. VAT is charged at a standard rate of 5%. Both create predictable, dated outflows. That is exactly the kind of bill a reserve and a forecast exist to handle. Payroll is paid through the Wage Protection System, the salary-transfer system run by the Ministry of Human Resources and Emiratisation, so the payroll layer must always stay liquid. For the detail on registering and filing, see our corporate tax registration and UAE VAT articles.

One bank or several? Settling the question for new UAE businesses

A common argument says a business should spread its money across several banks. The idea is that if one account is frozen, operations continue. That logic holds for large companies with complex, high-volume operations and the staff to manage many banking relationships. For a new UAE business, it usually creates more problems than it solves.

Opening several accounts at once can itself raise risk flags during compliance review. Each account has its own activity expectations, its own reviews, and its own paperwork. Spread a modest balance across all of them, and each one can look underused. And the protection most founders want is not about multiple banks at all. It is about keeping personal money separate from business money. It is also about keeping liabilities, such as VAT, tax, and payroll, separate from working capital. All of that fits inside one well-run business account.

So the honest answer for most new businesses is simple: one well-managed business account is enough. Revisit the question only when the business genuinely outgrows it.

Signals you have outgrown a single account

A second banking relationship makes practical sense in a few cases. One is when you regularly trade in several currencies and pay conversion costs you could manage better. Another is when monthly transaction volume is high enough that one account's limits create friction. A third is when you have operations or clients abroad that an international bank serves better. Until one of those is true, a second account is overhead, not insurance.

How cash flow forecasting keeps you ahead of trouble

A bank account records what already happened. A cash flow forecast shows what is about to happen. For a new business, cash flow forecasting turns cash flow management from reaction into planning. It is simpler than it sounds.

A forecast is a rolling view of expected cash in and cash out, week by week, for the next one to three months. You set known inflows, such as invoices due and expected sales, against known outflows, such as rent, salaries, supplier payments, VAT due, and loan repayments. Then you watch the running balance. The value is not precision. It is a warning. When the forecast shows a dip three weeks out, you still have three weeks to act. You can chase an overdue invoice, delay a non-urgent purchase, or arrange short-term financing calmly instead of in a panic.

Cash flow management and forecasting work as a pair. Management is the daily discipline of controlling what moves. Forecasting is the forward view that shows where that discipline needs to focus. A spreadsheet is enough to start. What matters is updating it every week, so it reflects what is really happening.

Two honest caveats. A forecast is only as good as its inputs. A business with unpredictable sales should forecast a shorter horizon and update it more often. And the further out you look, the less reliable the forecast becomes. Projecting four to six weeks accurately beats guessing at six months.

When a corporate account application is rejected: how to recover

Even with good preparation, rejections happen. They are most common for activities a bank treats as high risk. A rejection is a setback, not a dead end. What it must not become is a cash flow crisis. Whether it does depends almost entirely on how fast it is resolved.

One Best Solution client ran an international trading business under a general trading and commercial brokerage licence. The bank rejected the corporate account application for two reasons. The activity was treated as high risk. And the supporting documents for the client's company in his home country were incomplete at submission. The consequence was immediate. With no account to receive customer payments, incoming cash stopped. That quickly began to threaten supplier payments and daily operations.

The recovery had two parts. The first was finding out exactly what the bank's compliance team was worried about, instead of guessing. The second was rebuilding the application around those concerns. That meant a complete, well-structured set of supporting documents: proof of business activities, source of funds, contracts, invoices, and the home-country company documents. It also meant a clearer presentation of the business model. With that file in place, an alternative banking solution was secured, suited to the activity. The client resumed operations and stabilised cash flow.

The lesson for any new business is simple. A rejection is usually a documentation and presentation problem, not a verdict on the business. Act quickly. Understand the specific objection. Do not let the gap stretch into missed supplier payments. That is what keeps a banking setback from turning into a cash flow failure.

UAE banks apply this scrutiny for a reason. They operate under a strict anti-money-laundering regime. Federal Decree-Law No. 20 of 2018 on Anti-Money Laundering, supervised through the Central Bank of the UAE, requires banks to verify business activity, ownership, and source of funds carefully. The scrutiny is regulatory, not personal. Knowing that makes it easier to prepare for.

Banking Essentials for UAE Businesses

Getting your banking right before cash flow becomes the problem

Cash flow problems in a new UAE business are rarely sudden. They build quietly from banking decisions made at setup. And they are almost always preventable. The businesses that stay liquid through year one are not the ones with the most revenue. They are the ones that separated their accounts, prepared their banking properly, and could see pressure coming.

Best Solution has spent 23 years helping more than 5,000 businesses set up in the UAE. It has opened over 4,500 corporate bank accounts, with about 90% approved on the first attempt. If you are setting up a company, speak with Best Solution's banking and tax consultants before the first cash flow squeeze, not after it. For account opening support, see our bank account opening assistance article.

Secure External Capital Facility as Buffer

The one strategy I'd insist on is decoupling your operational banking from your strategic capital. Too many founders treat their local Dubai bank account as their entire financial backbone, which is a massive single point of failure. When a payment is delayed or an unexpected cost arises, their operations can seize up instantly because their only source of liquidity is tied to daily cash flow.

The smarter approach is to secure a line of credit or a capital facility from an institution outside the UAE before you even finalize your local setup. This isn't for payroll; it's your emergency reserve. This strategy provides a critical buffer against local market volatility and, just as importantly, signals stability to your Dubai bank.

Founder, Unicorn Innovations

Establish Flexible Multi-Currency Banking Solutions

When finalizing a business setup in Dubai, the one strategy I'd insist on is establishing flexible access to both operational and contingency capital from day one. This means opening a bank account that supports multi-currency transactions, online banking, and credit facilities, while also maintaining a clear line of sight on cash flow forecasts.

The reason is simple: liquidity roadblocks are one of the fastest ways operations stall, whether it's delayed vendor payments, missed payroll, or unexpected market opportunities. By carefully planning capital access—combining operational accounts with short-term financing options or corporate credit lines—you create a buffer that allows the business to operate smoothly and respond quickly to growth or challenges.

The key takeaway: in Dubai's fast-moving business environment, proactive financial infrastructure isn't just administrative—it's a strategic safeguard that keeps your business agile and resilient.

CEO, EDS FZE

Build Substantial Cash Reserves Before Debt

Based on my experience in real estate development, I strongly recommend establishing a substantial cash reserve before taking on any significant debt obligations when setting up your business in Dubai. This strategy proved invaluable during my early Las Vegas project when unexpected repair costs arose. Still, our cash reserves allowed us to handle these surprises without missing loan payments or experiencing cash flow problems. Having this liquidity buffer is particularly important in Dubai's fast-paced business environment, where operational delays can quickly impact your market position. A proper cash reserve gives you both stability and the flexibility to navigate unforeseen challenges while maintaining your regular operations.

Founder, Fast Vegas Home Buyers

Partner with Bank for Cash Flow Forecasting

When establishing your business in Dubai, I recommend partnering with a bank that offers robust cash flow forecasting capabilities. Based on my experience, implementing a dynamic cash flow model that updates in near real time enabled our business to anticipate financial challenges weeks before they materialized. This proactive visibility enabled us to make timely decisions, such as adjusting hiring timelines or working with clients on payment schedules, ultimately preventing the liquidity constraints that often challenge new market entrants.

Managing Consultant and CEO, Spectup

Diversify Banking Relationships to Mitigate Risk

When finalizing your business setup in Dubai, the one banking strategy you must insist on is establishing relationships with multiple banks rather than relying on a single institution that could freeze your operations overnight.

Dubai's banking environment is challenging: 50% of corporate account applications are rejected in the UAE, and accounts can be frozen due to enhanced compliance scrutiny, changes in risk classification, or documentation discrepancies. Single-bank dependency is extremely dangerous.

Here's my recommended framework: First, establish your primary operating bank with a major UAE institution, such as Emirates NBD or Mashreq, for credibility and digital capabilities. Second, secure a backup relationship with an international bank like HSBC or Standard Chartered operating in Dubai. Third, obtain an emergency credit facility with a third institution before you need it.

The key is strategic implementation. Don't open multiple accounts simultaneously, as this triggers risk flags. Open your primary account first, establish a 6-month track record, then approach secondary banks. Maintain minimum balances across institutions rather than concentrating funds in one bank, and ensure all banks receive identical documentation.

Beyond traditional banking, diversify with trade finance facilities, digital payment solutions, and pre-qualified Islamic financing products. Assign dedicated relationship managers at each institution and maintain quarterly communication to update them on business developments.

This multi-bank strategy provides essential liquidity protection when compliance issues or policy changes threaten to paralyze your operations.

Managing Director, BMA Business Solutions GmbH