If you run a small business in the UAE, you have probably heard that the VAT rules change in 2026. The good news: the headline rate is not going up. The standard VAT rate stays at 5 percent, and zero-rating, exemptions and VAT group rules are untouched. What changes is the paperwork and the deadlines around how you account for VAT, reclaim it, and protect your right to a refund. Get those wrong and a legitimate refund can quietly expire. Get them right and you cut admin, free up cash, and avoid penalties.

Here is the plain-English version: what is actually changing under Federal Decree-Law No. 16 of 2025, when each rule starts, and a short checklist to get your business ready before 1 January 2026.

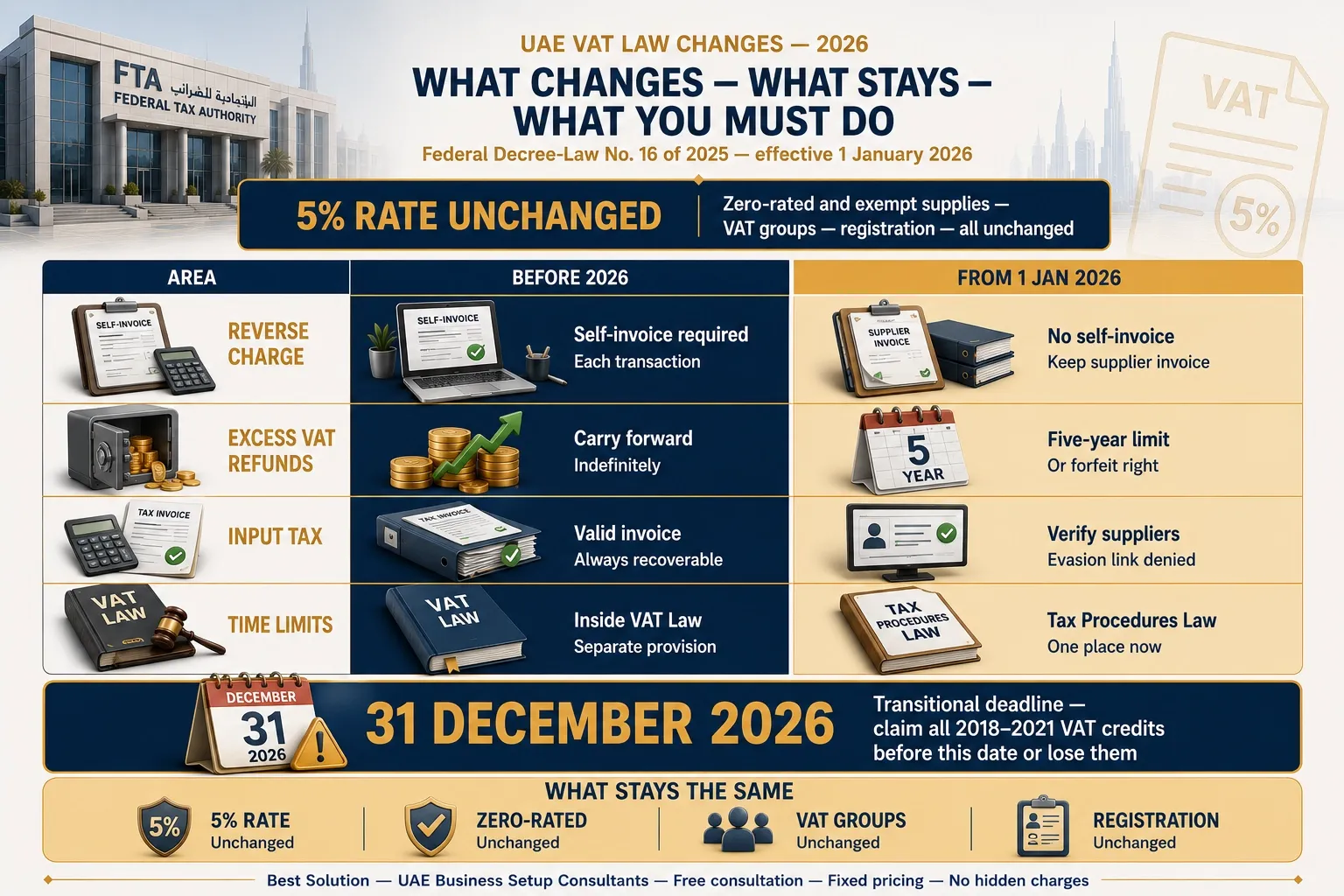

The 2026 UAE VAT changes at a glance

| What Changed | What It Means for You |

|---|---|

| Self-invoicing scrapped under reverse charge | No more internal self-invoices for imports; just keep the supplier invoice and import documents[cite: 1]. |

| Five-year limit on reclaiming excess VAT | Claim or use excess VAT credits within five years, or you lose them[cite: 1]. |

| Input tax denied if linked to evasion | Verify your suppliers; the FTA can refuse your input VAT if a supply is tied to evasion and you should have known[cite: 1]. |

| VAT time limits move to the Tax Procedures Law | Audit and assessment deadlines now sit in one place, under Decree-Law No. 17 of 2025[cite: 1]. |

| Effective date | 1 January 2026 (key transitional deadline: 31 December 2026)[cite: 1]. |

What are the new VAT rules in the UAE for 2026?

Quick answer

From 1 January 2026, the UAE updates its VAT Law under Federal Decree-Law No. 16 of 2025. Four things change: businesses stop issuing self-invoices under the reverse charge mechanism, a strict five-year limit applies to reclaiming excess VAT, the Federal Tax Authority can deny input tax linked to evasion, and VAT time limits move into the Tax Procedures Law. The 5 percent rate is unchanged.

When do the new UAE VAT rules take effect?

The amendments take effect on 1 January 2026. They were issued in 2025 by the UAE Ministry of Finance as Federal Decree-Law No. 16 of 2025, amending the original VAT Law (Federal Decree-Law No. 8 of 2017). A linked update, Decree-Law No. 17 of 2025, amends the Tax Procedures Law on the same date. The single most important date to circle is 31 December 2026: the cut-off for the transitional refund window explained below.

The four key VAT changes, explained

Here is each change, what happened before, and what you do now.

| Area | Before 2026 | From 1 Jan 2026 |

|---|---|---|

| Reverse charge | Issue an internal self-invoice for each reverse-charge supply | No self-invoice; retain the supplier invoice and import documents |

| Excess VAT refunds | Carry forward credits indefinitely | Claim or use within five years of the tax period, or forfeit |

| Input tax | Recoverable on a valid tax invoice | Denied if the supply is linked to evasion and you should have known |

| Time limits | Set inside the VAT Law | Moved into the Tax Procedures Law (Decree-Law No. 17 of 2025) |

1. No more self-invoicing under the Reverse Charge Mechanism

The reverse charge mechanism (RCM) shifts the duty to account for VAT from the supplier to you, the buyer. It applies most often when you import goods or services from a supplier based outside the UAE: you record the VAT as output tax and reclaim it as input tax in the same return, so the net cash effect for a fully taxable business is usually zero. It exists so the government still captures VAT on services consumed in the UAE without forcing every foreign supplier to register here.

Until now, RCM meant creating an internal self-invoice for each transaction, duplicating information already in your customs declaration or the supplier's invoice. From 2026 that step is gone. You simply keep the original supplier invoice and import documentation as evidence. Less paperwork, fewer manual errors, and a cleaner audit trail, provided you retain the supporting documents the Executive Regulation requires.

2. A five-year limit on reclaiming excess VAT

Under the amended Article 74(3), excess recoverable VAT can be carried forward for a maximum of five years from the end of the tax period in which it arose. If, within those five years, you neither use the credit to offset a VAT liability nor submit a refund request, the right to recover it lapses for good. Importantly, it is the act of submitting the refund request (or using the credit) that protects it; the refund does not have to be paid out within the five years.

Watch this deadline

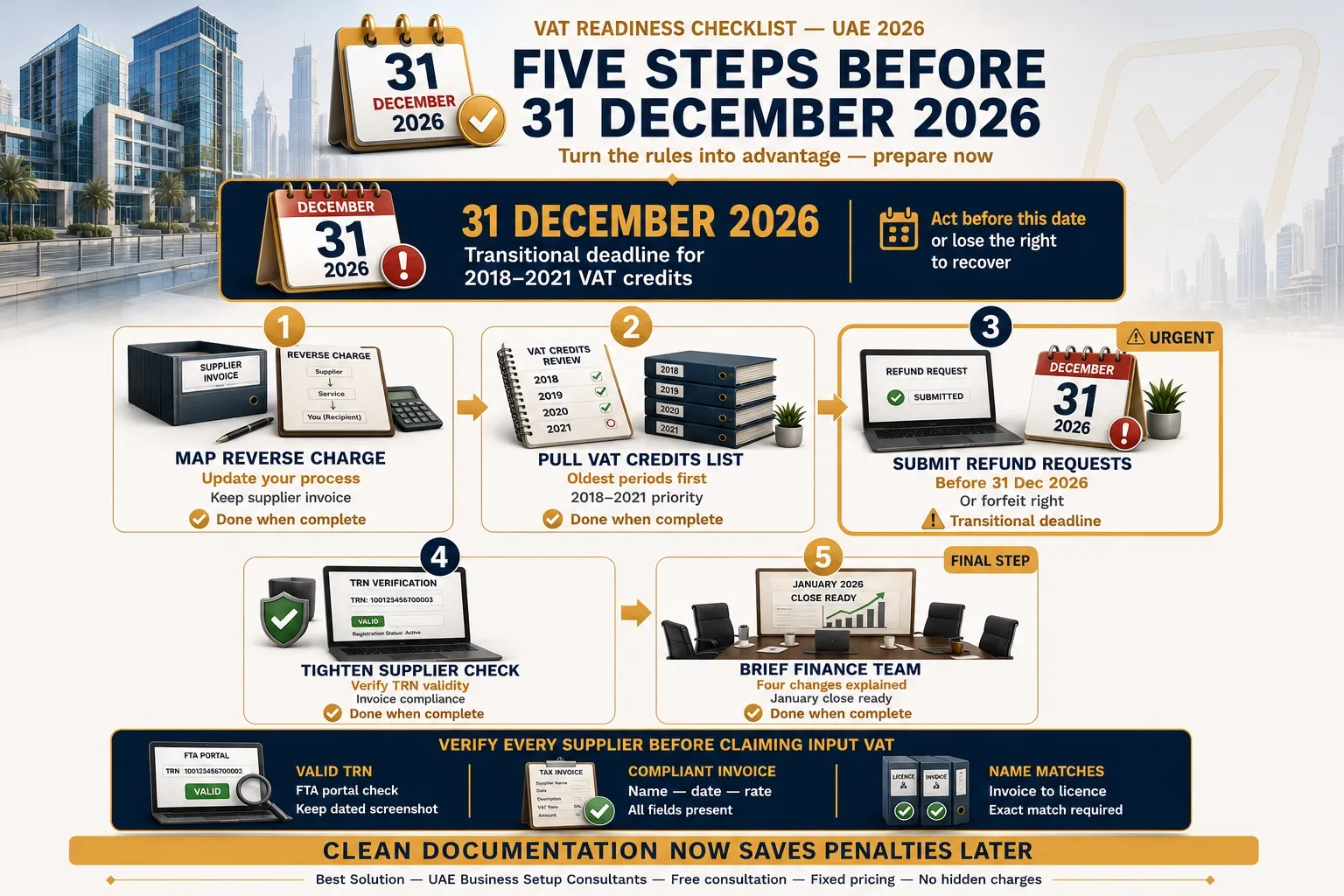

Transitional relief lets businesses whose five-year period has already expired, or expires within one year of 1 January 2026, submit outstanding claims up to 31 December 2026. In practice, older credits from the 2018-2021 tax periods should be reviewed now: every 2021 credit will have lapsed by 31 December 2026 if no action is taken. If you are sitting on dormant VAT credits, this is the rule that can quietly cost you money.

3. Stricter denial of input tax linked to tax evasion

The amendments authorise the Federal Tax Authority (FTA) to deny your input tax deduction where a supply, or a chain of supplies, is connected to a tax-evasion arrangement and you knew, or reasonably should have known, at the time you claimed it. Before 2026, input VAT was generally recoverable on a valid tax invoice alone. Now your vendor due diligence is part of your VAT defence: you are expected to verify the legitimacy of suppliers, the integrity of transactions, and compliance across your supply chain. It is a shared-responsibility model, and it makes clean supplier records a cash-flow protection, not just an admin chore.

4. The VAT statute of limitations moves to the Tax Procedures Law

This is the change most short summaries miss. The VAT Law no longer contains its own standalone provision for time limits on audits, assessments and related actions. Those rules have been repealed from the VAT Law and consolidated into the UAE's broader Tax Procedures Law, amended in parallel by Decree-Law No. 17 of 2025. Nothing about your day-to-day VAT changes here, but it matters: from 2026 you look in one place, the Tax Procedures framework, to understand how long the FTA can review your filings. Big-Four analysis from KPMG notes the Tax Procedures changes are actually the more substantial of the two laws.

What has not changed in 2026

It is just as important to know what stays the same, so you do not over-correct:

- The 5 percent standard rate is unchanged.

- Zero-rated and exempt supplies keep their existing treatment.

- VAT group rules are not affected.

- Your obligation to register for VAT and stay compliant continues exactly as before.

How the new VAT rules affect entrepreneurs and small business owners

Whether you are a startup founder in Dubai, a trading firm in Sharjah, or a consultant serving expat investors, the 2026 rules land in three practical ways:

- Less admin, better cash flow. Removing the self-invoice step frees up time and reduces clerical errors, so your team spends less of the month on VAT housekeeping.

- Refund certainty, with a clock. The five-year window stops working capital tying up indefinitely, but it also means you have to track credits by tax period and act before they expire. Tight cash-flow management now includes a VAT-credit calendar.

- More responsibility for due diligence. Before you deduct input VAT, you are expected to confirm the supply is legitimate. That means stricter vendor checks and tidy documentation.

Your 2026 VAT readiness checklist

Five steps will put most SMEs in a strong position well before the deadline:

- Map your reverse-charge transactions and update your process so you keep supplier invoices and import documents instead of generating self-invoices.

- Pull a list of all excess VAT credits by tax period, oldest first, and flag anything from 2018-2021.

- Submit refund requests, or offset credits, before 31 December 2026 for any balance approaching its five-year limit.

- Tighten supplier onboarding with a TRN and tax-invoice check (below).

- Brief your finance team or bookkeeper on the four changes so nothing slips in the January 2026 close.

Verify every supplier's TRN before you pay

Because the FTA can now deny input tax tied to evasion, supplier verification is your first line of defence. Before you pay a new vendor: confirm their Tax Registration Number (TRN) is valid and registered with the FTA (keep a dated screenshot), check that the tax invoice is fully compliant (legal name, address, date, VAT rate and amount), and make sure the name on the invoice matches their trade licence. Our step-by-step guide on how to check TRN validity in the UAE walks through the FTA verification tool.

Reconcile and claim refunds before they expire

Treat the five-year limit as a recurring reconciliation task, not a one-off. Review historical balances, prioritise the oldest credits, and either offset them against a VAT liability or file a refund request in time. If you are unsure which credits are at risk, a VAT refund review can map your exposure quickly.

What Best Solution is seeing on the ground

This is where the 2026 changes get real. According to our internal audit data for 2024, 38 percent of our small and medium-sized enterprise clients reported at least one administrative error in issuing or documenting self-invoices under the reverse charge mechanism. Removing that requirement is, on our numbers, expected to cut RCM-related compliance errors by up to 35 percent for those clients from 2026. That is a direct saving in both time and risk for the average entrepreneur.

From our CEO

“These new VAT laws in the UAE bring clarity and simplify compliance, but they also demand better internal controls. Small businesses should start preparing now: clean documentation and supplier verification will be essential to avoid penalties.”

CEO, Best Solution

From our General Manager

“By removing redundant paperwork and setting sensible limits on refunds and deductions, entrepreneurs can forecast cash flow with more certainty and avoid pitfalls. For any small business looking to scale responsibly in the UAE, that is a welcome mix of simplicity and accountability.”

General Manager , Best Solution

Conclusion: turn the 2026 rules into an advantage

The UAE's 2026 VAT update is less a burden than a tidy-up: less redundant paperwork, clearer refund timelines, and a stronger, fairer system. The businesses that benefit most are the ones that prepare early, keep clean documentation, verify their suppliers, and reconcile their VAT credits before the December 2026 deadline.

Get a free VAT-compliance review

Want to know exactly how the 2026 rules apply to your business and which VAT credits you should protect before they expire? Book a free, personalized VAT-compliance review with Best Solution and we will map your readiness in plain English.